What Must a Motor Dealer do to get IGF Cover?

In Brief

In order for a Motor Dealer to get IGF cover they must:

- Determine the Amount of the Cover Required

- Satisfy the Solvency Requirements

Determine the Amount of the Cover Required

The Short Term Insurance Act 1998 requires a motor dealer to have IGF cover for an amount equal to 30% of the gross premiums collected in the preceding year. This means that if the dealership collected R1 000 000 gross premiums last year, it must have IGF cover for R300 000.

Satisfy the Solvency Requirements

The solvency requirements for any person who wishes to obtain IGF cover are stringent.

IGF Net Income Requirements

The maximum guarantee that will be issued by the IGF is an amount equal to ten times the net annual income of the motor dealers business. Net income before tax will be adjusted for significant directors' emoluments and administration fees and a ratio of 10 will be applied to the result.

In other words, the adjusted annual net income of a dealership with its own FSP licence must be not less than R100 000.

IGF Net Current Assets Requirement

If the net income is found to be sufficient, the dealerships net current assets must not be less than 20% of the amount of the guarantee required.

Current assets are assets that can be liquidated or converted to cash within a year.

These include:

- Cash

- Marketable securities (cash in temporary stock or bonds)

- Account receivables (debts our customers owe us)

- Inventory

- Supplies

- Prepaid expenses- for example, if we paid insurance for the entire year in advance, then after 6 months we still technically have half of that payment in assets.

In other words, the net current assets of a dealership with its own FSP licence must be not less than R200 000.

For more details, please contact:

Intermediaries Guarantee Facility Limited

Ground Floor ,Willowbrook House, Constantia Office Park, C/O 14th Avenue & Hendrik Potgieter Street, Weltevreden Park

Telephone: +27 11 726 5381

Fax: 086 647 2276

Email: info@saia.co.za

Website: http://igfsec45.co.za

Is there an Alternative to IGF Cover?

In short the answer is YES – but the alternative is very strictly defined.

A motor dealer may ask a bank to issue a guarantee instead of making any application to the IGF.However, it is essential that the bank issue the guarantee in a very specific format. The Regulations (see below) provide that the bank guarantee must be issued in the format determined by the Registrar. This format was given in Board Notice 192 of 1998 in a Government Gazette dated 24th December 1998. A copy can be viewed here.

The guarantee must be issued in respect of the obligations of the motor dealer.

The Regulations in question are set out below. Please note that an "independent intermediary" means a person who renders services as intermediary and "services as intermediary" means any act performed by a person the result of which is that another person will or does or offers to enter into, vary or renew a short-term policy or any act performed by a person with a view to collecting or accounting for premiums payable under a short-term policy.

Regulation 4.1 Authorisation

-

A short-term insurer may, subject to subregulation (2), in writing authorise an independent intermediary to receive, hold or in any other manner deal with premiums payable to it under short-term policies.

-

A person shall not be authorised, as contemplated in subregulation (1),

unless that person has provided security, to the extent and in accordance with the requirements of this Part, in respect of his or her obligations in terms of regulation 4.3

by means of—

-

a guarantee policy issued by a short-term insurer registered to do so in accordance with a guarantee facility created by short-term insurers generally for the purposes of providing such security; or

- a contract which, but for the fact that the undertaking concerned is given by a bank, would be a guarantee policy, and under which policy benefits are to be provided in the event of the failure of that person to meet those obligations.

-

a guarantee policy issued by a short-term insurer registered to do so in accordance with a guarantee facility created by short-term insurers generally for the purposes of providing such security; or

Regulation 4.2 Requirements in respect of security

The security referred to in regulation 4.1 (2) shall—

-

be in such form as prescribed by the Registrar;

-

be in favour of the South African Insurance Association (Association Incorporated under Section 21) or, if the Registrar so determines, in favour of the Registrar, for the benefit of all of the short-term insurers with whose authority the premiums are received, held or in any other manner dealt under by the person concerned;

-

be provided, before any premium is received, held or in any other manner dealt with by the person concerned;

-

be provided, and renewed annually, in respect of each financial year of the person concerned;

-

subject to paragraph (f), be for an amount equal to-

-

in the first two financial years in which the person concerned is authorised to receive, hold or in any other manner deal with premiums,

30 percent of a reasonable estimate of the total premiums which that person expects to receive in that financial year; and

-

in any other financial year of the person concerned, 30 percent of the total premiums actually received, held or in any other matter dealt with by that person in the previous financial year; and

-

in the first two financial years in which the person concerned is authorised to receive, hold or in any other manner deal with premiums,

30 percent of a reasonable estimate of the total premiums which that person expects to receive in that financial year; and

-

if the businesses of two or more independent intermediaries are amalgamated, be for an amount determined by reference to the total premiums received, held or in any other manner dealt with in the financial year concerned by the businesses so amalgamated,

- Despite paragraph (e), the amount referred to in paragraph (e) may not be less than R100 000 . . . etc

Summary

The significance of this is that a motor dealer who collects premiums on short term insurance products falls within the definition of an independent intermediary. It matters not whether he is a juristic representative of some other entity for FAIS purposes or whether he is a member of some or other Umbrella Scheme: if he collects premiums he must have IGF or an alternative form of cover.

In essence then, if a motor dealer is able to obtain a guarantee from a bank, the guarantee must be in the form of the as set out in Board Notice 192 of 1998 and must be in favour of the Dealership generally.

It is not possible to limit the guarantee to premiums collected for any nominated insurer or warranty provider. The guarantee is in respect of any and all premiums that may be collected by the dealership.

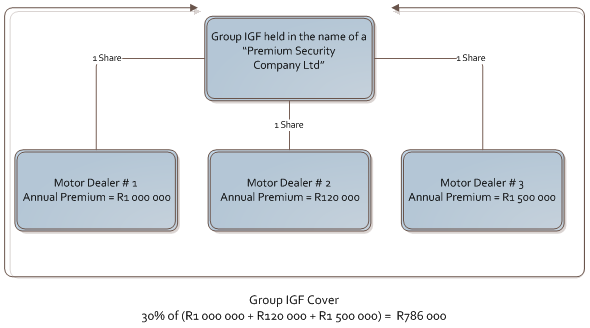

Group IGF Cover - Is It Possible?

There are structures that have been established in an attempt to assist motor dealers to continue to receive premiums without having to go to the enormous trouble of finding adequate IGF cover.

These Group Schemes all require motor dealers to buy shares in a dedicated special purpose company.

IGF AND GROUP SCHEMES

Group or collective security is only considered to meet the requirements of Regulation 4.1 (2) if:

- each motor dealer member and the security held in respect of that motor dealer 's obligations are individually identified;

- the security held collectively is equivalent to the sum total of that which would need to be held on behalf of each and every so identified motor dealer;

- the security held must relate to all premiums collected by each and every so identified motor dealer and not only to the premiums collected on behalf of a specific insurer. To further clarify, this means that if a motor dealer collects premiums on behalf of insurer A and insurer S, the security held must cover the premiums collected on behalf of both insurers A and Sand cannot only cover premiums collected on behalf of insurer A; and

- the group of motor dealers on whose behalf the collective security is held, whether incorporated or unincorporated, may not self-insure by paying premiums to an insurer on behalf of a defaulting motor dealer, without calling the bank guarantee or instituting a claim under the guarantee policy.

The IGF cover held in such Premium Security Schemes will only be valid and effective if the following additional conditions are met:

- Each motor dealer who collects premiums must be specifically referred to in the IGF policy.

- The amount of the cover must be equal to 30% of ALL premiums collected by ALL motor dealers who participate in the Scheme

- Each motor dealer who collects premiums must be specifically authorised in writing each insurer on whose behalf premiums are collected.